What is Self-Funded Insurance?

Under a self-funded or self-insured health plan, employers fund the plan rather than paying a premium to a commercial insurer. This means taking on the responsibility – as well as the risks and rewards of paying the medical and prescription drug claims of employees and their families.

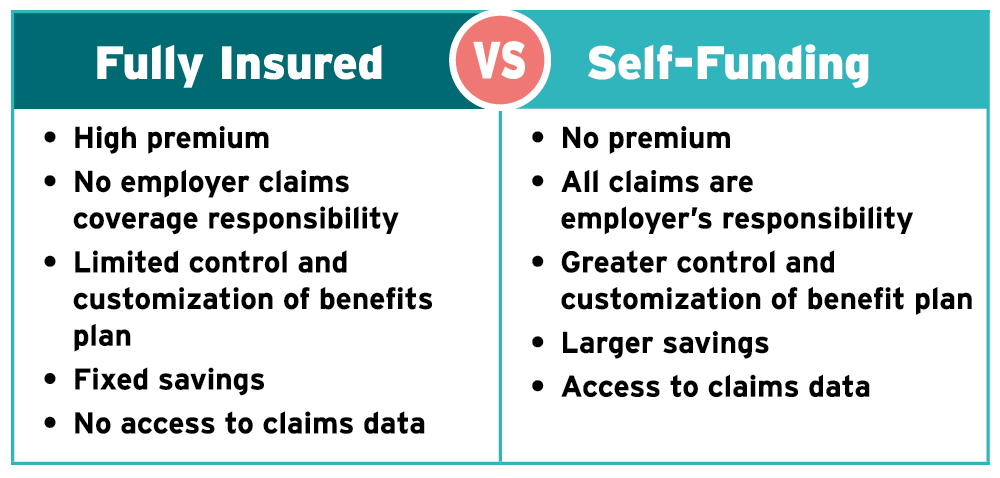

Self-funding can be a better alternative to the traditional fully insured approach, driving greater transparency, control, and cost savings.

The Smarter Alternative to Traditional Health Plans

Anyone can self-fund! Businesses, unions, Taft-Hartley Insurance Trusts, municipalities, school districts, and other types and sizes of organizations have successfully self-funded with The Alliance. We’ll help you every step of the way towards self-funding success.

The Alliance Way

Why Self-Funded Insurance?

You may be interested in self-funded insurance because you’re frustrated with healthcare as usual. Other insurers make few attempts to improve network quality and employer savings. But at The Alliance®, we’re an advocate for our employers, and our primary focus is designing Smarter NetworksSM that drive Serious Savings.

When you choose self-funded insurance with The Alliance, you get better care at a better price.

Self-Fund with The Alliance

Get the best care at the best price. When you join The Alliance, we help you develop custom, high-value provider networks that optimize quality and savings. After the health of your employees and their families, our main focus is your bottom line.

Our 425+ Clients Enjoy These Benefits

Frequently Asked Questions

What is self-funded insurance?

In a self-funded or “self-insured” health plan, the business or other organization accepts responsibility for the risk of healthcare for enrollees, who are typically employees and family members. The business self-funds the plan rather than paying a premium to a commercial insurer.

What is The Alliance’s role in self-funding?

Our employer-members purchase stock in The Alliance (to join the not-for-profit cooperative) and pay small fees for our services and access to our Smarter Networks – which encompass 38,000 hospitals, physicians, specialists, and other providers.

The Alliance uses its purchasing power to contract directly with those providers at significantly lower rates (that are almost always contracted as a percentage of Medicare). By joining The Alliance, employer-members also enjoy discounts to our benefits partners, access to regular events and webinars, employee education and outreach initiatives, health policy advocacy, and the opportunity to network and learn from other self-funded employers.

What types of organizations can choose self-funded insurance?

Self-funding has been used successfully by many types of organizations including businesses, unions, Taft-Hartley Insurance Trusts, municipalities, and school districts.

What is the minimum size an employer or organization must be to self-fund?

In recent years, smaller organizations have pursued self-funding. A typical rule of thumb is that a business should have at least 100 covered lives to effectively self-fund; however, organizations with roughly 30 employees have recently chosen to self-fund. Any organization that provides health benefits and is willing to fulfill the legal and fiduciary responsibilities of self-funding can pursue this option. Data analysis is essential to discover whether self-funding is a wise choice for your health benefit plan.

What types of health-related benefits can be self-funded?

Five types of health-related benefits are often self-funded:

- Medical

- Prescription drugs

- Short-term disability

- Dental

- Vision

What rules cover self-insured benefits?

Self-funded health benefits must primarily comply with the Employee Retirement Income Security Act of 1974 (ERISA). This a federal law that sets minimum standards for most voluntarily established pension and health plans in private industry to provide protection for individuals in these plans.

How do I protect my company from high claims?

Companies purchase stop-loss insurance to protect their financial health.

What is stop-loss insurance?

Stop-loss insurance is purchased from an insurance carrier to cap catastrophic claims risk. This insurance reimburses the business that sponsors the health plan when claims exceed a predetermined level for either an individual or the entire group. Coverage for individual claims is known as “specific coverage” while coverage for group claims is known as “aggregate coverage.”

What vendor relationships are required to assist a business with self-funded insurance?

A business that uses self-funded insurance will typically need to use the services of a:

- Third-party administrator to administer the plan. This may include implementing the plan design, bidding for stop-loss coverage, maintaining enrollment records, paying claims, and working with the provider network and other vendors.

- Agent/broker to assess the employer’s needs and help find solutions.

- Provider network to negotiate contracts with doctors, hospitals, and other health services.

- Stop-loss carrier to protect the employer from high financial claims.

- Wrap network to cover enrollees who travel or study outside the standard provider network.

In addition, employers may choose to use a:

- Pharmacy benefit manager (PBM) to negotiate discounts for prescription drugs.

- Health savings account (HSA) Administrator to administer accounts linked to high deductible health plans (HDHPs).

- Case management firm

- Disease management firm

- Wellness program vendor

- Care coordination firm

How do self-funded businesses develop an effective plan design?

Organizations providing self-funded health benefits should work with a broker or consultant to develop a health benefit plan design that will address four areas:

- Customized benefits that meet the needs of the business as well as the workforce.

- Coverage and exclusions, which provide control over what is, and is not, covered by the plan.

- The plan’s relationship to larger goals for employee well-being. For example, a wellness-based plan may pay higher levels for preventive care if employees participate in a health risk assessment.

- The role of health benefits in long-term strategy, which includes employee recruitment and retention needs.

How do people covered by the plan know what is covered?

Under ERISA, the organization providing the self-funded plan must create and distribute a Summary Plan Description (SPD) that is a clear and complete source of information for employees. The SPD must detail eligibility provisions, the benefits available, and how coverage is terminated or denied. The SPD serves as a contract between the employer and employee and is used by the claim administrator and stop-loss carrier to administer claims. The Affordable Care Act (ACA) also requires self-funded plans to provide a shorter Summary of Benefits and Coverage (SBC) that is drawn from the SPD. There are specific requirements for the length, contents, and format of the SBC.

Want to network with executives and human resources leaders from other self-funded businesses to find out how it really works?

Attend an Event by The Alliance. Our free educational events feature national and regional experts in health and health benefits and are open to all employers — even those that are not part of The Alliance.